Fees Keep Nearly a Third of Small Businesses From Instant Pay Adoption

Small business owners often see instant payments as the fix for sluggish cash flow.

However, the PYMNTS Intelligence report “Immediate Impact: How SMBs Can Benefit From Instant Payments” suggests the technology is deepening a growing divide between digital haves and have-nots.

While instant payments adoption is rising, its benefits are pooling in a narrow band of industries that already lead in digital transformation. Firms in gaming, gig work and other digital-first sectors have moved ahead, leaving behind the millions of small- to medium-sized businesses (SMBs) still reliant on checks, manual reconciliation and outdated accounts receivable systems.

Instant payments access has become a new marker of digital momentum, and by extension, competitiveness. Instant payments now account for a larger share of ad hoc transactions, which are one-off, non-recurring payments that have become central to SMB liquidity.

Instant payments access has become a new marker of digital momentum, and by extension, competitiveness. Instant payments now account for a larger share of ad hoc transactions, which are one-off, non-recurring payments that have become central to SMB liquidity.

According to the report, 55% of SMB accounts receivable transactions are now ad hoc, representing 69% of total AR volume in dollars. Thirty-two percent of SMBs received those payments through instant methods in August 2024, up from 20% in September 2023.

It’s a sign of headline growth but also of how quickly the gap is widening between industries able to modernize and those still constrained by legacy systems.

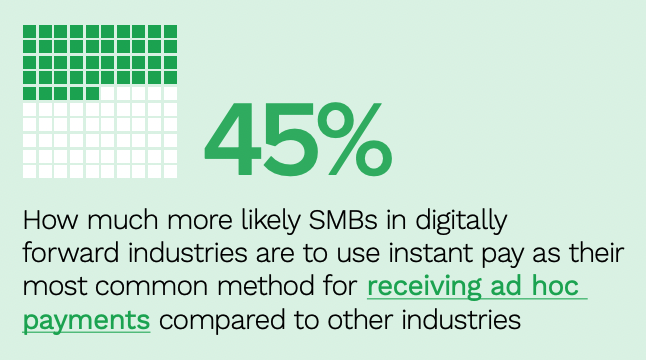

- SMBs in digitally forward industries such as gaming and the gig economy are 45% more likely than other sectors to use instant payments as their most common method for receiving ad hoc payments.

- Improved cash flow is cited by 73% of microbusinesses as their top reason for adopting instant payments, up 18% from seven months earlier.

- The share of SMBs declining instant payments options due to the associated fees increased by 53%, with roughly 32% of SMBs citing fees as the main reason for avoiding instant payments options.

Beneath the surface of instant payments growth lies a subtler finding. Automation, not just adoption, determines who reaps the benefits. The report finds that 37% of SMBs using automated AR systems receive ad hoc payments instantly compared to 24% of those relying on manual processes. The distinction matters. As more than 4 in 10 microbusinesses still handle AR manually, the report suggests that automation rather than raw demand may be the strongest predictor of financial agility.

In digitally mature sectors, instant payments tools are increasingly tied to broader embedded finance platforms. Trustly’s new Pay N Play technology, for example, trims gaming transaction times to less than 10 seconds and boosts average transaction values by 10%. Similar integrated systems, such as QuickBooks’ Tap to Pay on iPhone, are allowing small firms to skip legacy rails entirely and close their own liquidity gaps in real time.

The report concludes that instant payments adoption isn’t just about speed; it’s about access. One-quarter of SMBs always opt for instant payments when available, but firms in lagging sectors say they are never offered an instant option at all. In other words, many small businesses aren’t rejecting instant payments. They’re being left out of the ecosystem that enables them.

“Removing complexity is key to unlocking the full impact of instant payments for SMBs,” said Drew Edwards, CEO of Ingo Payments, which collaborated on the report.

Until that happens, the instant payments revolution may look less like a leveler and more like the latest dividing line between digital leaders and the rest of Main Street.

The post Fees Keep Nearly a Third of Small Businesses From Instant Pay Adoption appeared first on PYMNTS.com.