Digital Onboarding Now Decides Credit Union Loyalty

Innovation is no longer a luxury but a defining factor for credit unions striving to thrive in the current financial ecosystem. As consumer and small to medium-sized business (SMB) expectations rapidly shift toward digital convenience and tailored experiences, credit unions face increasing pressure to modernize their offerings, not just to compete with traditional banks, but to maintain relevance.

[contact-form-7]At the forefront of this modernization is digital onboarding, as customers interact with CUs to open accounts and access services.

Top-performing credit unions leverage that digital point of contact to deepen member loyalty, grow market share, and unlock significant cross-selling opportunities.

The latest PYMNTS Intelligence “Credit Union Innovation Readiness Index,” done in collaboration with Velera, reveals a clear mandate for digital transformation, especially concerning member acquisition and engagement.

A Shift to Digital ChannelsWhile approximately half of credit union members still prefer to apply for new products in person, there’s a pronounced shift among key growth segments towards digital channels. For instance, Generation Z consumers rank digital onboarding 78% higher in importance than the average consumer, underscoring their digital-first mindset.

Similarly, 68% of SMBs that recently switched away from a credit union express a clear preference for online onboarding for new product applications. Millennials, too, show a strong inclination, with 52% expecting digital onboarding. These figures highlight that a lack of robust digital tools, including seamless digital onboarding, is a significant factor in member churn.

A Gateway to Cross-SellingFor credit unions, digital onboarding is more than just a convenience; it’s a strategic gateway to a deeper, more comprehensive digital relationship with members. Once a member is digitally onboarded, the credit union gains immediate access to a digital touchpoint, which can be leveraged for future cross-selling of additional products and services.

Top-performing credit unions understand this deeply, focusing on “building smarter” by aligning their innovation efforts closely with member expectations. They are not just offering more features, but features that truly resonate and drive satisfaction.

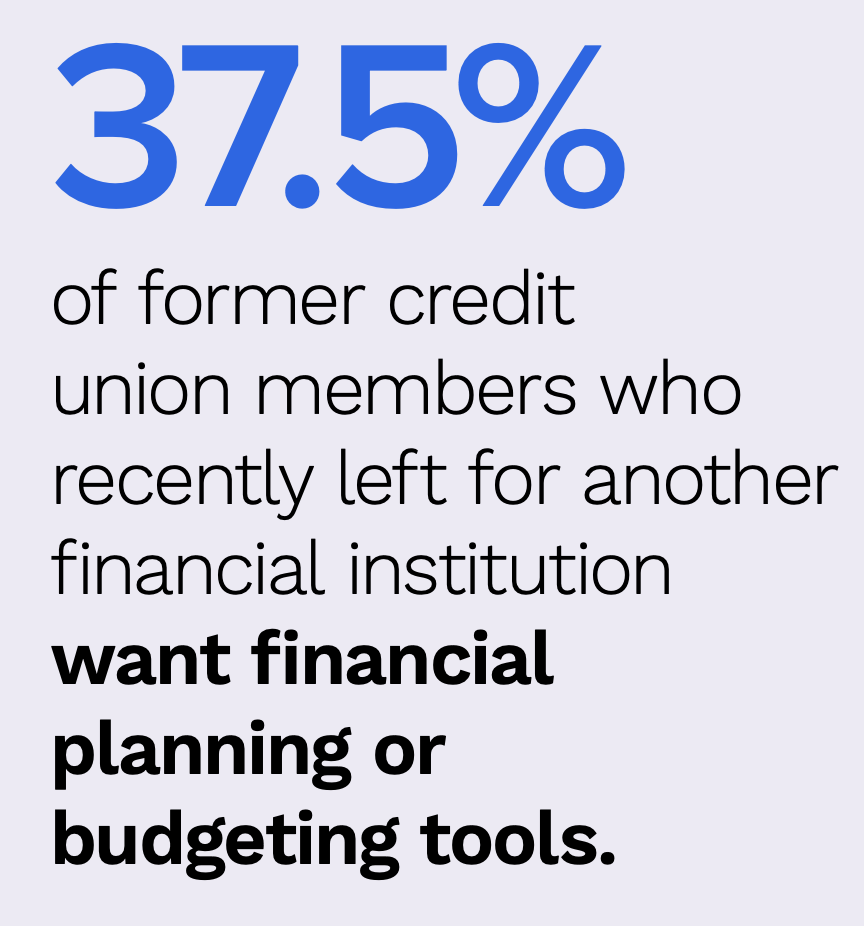

Data from the Index illustrates this approach. Top-performing credit unions are significantly more likely to offer crucial digital capabilities that complement digital onboarding. For example, they are 48% more likely to offer mobile credit card apps compared to bottom performers (48% versus 7%), and a staggering 86% offer open banking compared to only 13% of bottom performers. Budgeting tools also show a wide gap, with 53% of top performers offering them versus 27% of bottom performers.

While 40% of bottom-performing credit unions are still focused on launching new basic products, 47% of top performers are prioritizing new features that elevate the member experience.

The data show that through the next few years, 92% of top-performing credit unions plan to offer digital onboarding, 74% will enable instant card issuance and 85% will provide mobile credit card apps. This foresight ensures they can continue to meet rising member expectations and capitalize on opportunities to expand product usage. For instance, SMBs using credit union-issued cards as their primary payment method are 50% more likely to value loyalty programs, demonstrating how an initial digital relationship can be nurtured to encourage further engagement and product adoption.

Partnerships Are CriticalFinally, credit unions are not going it alone in this digital transformation. The report highlights the critical role of external partnerships. A remarkable 79% of all credit unions, including 83% of top performers, cite external partners as instrumental in helping them innovate faster and at greater scale.

The post Digital Onboarding Now Decides Credit Union Loyalty appeared first on PYMNTS.com.